COUNSEL'S

OPINION

DAVID EWART.

Pump Court Chambers, 16 Bedford Row, London, WC1R 4EB

27th September 1994.

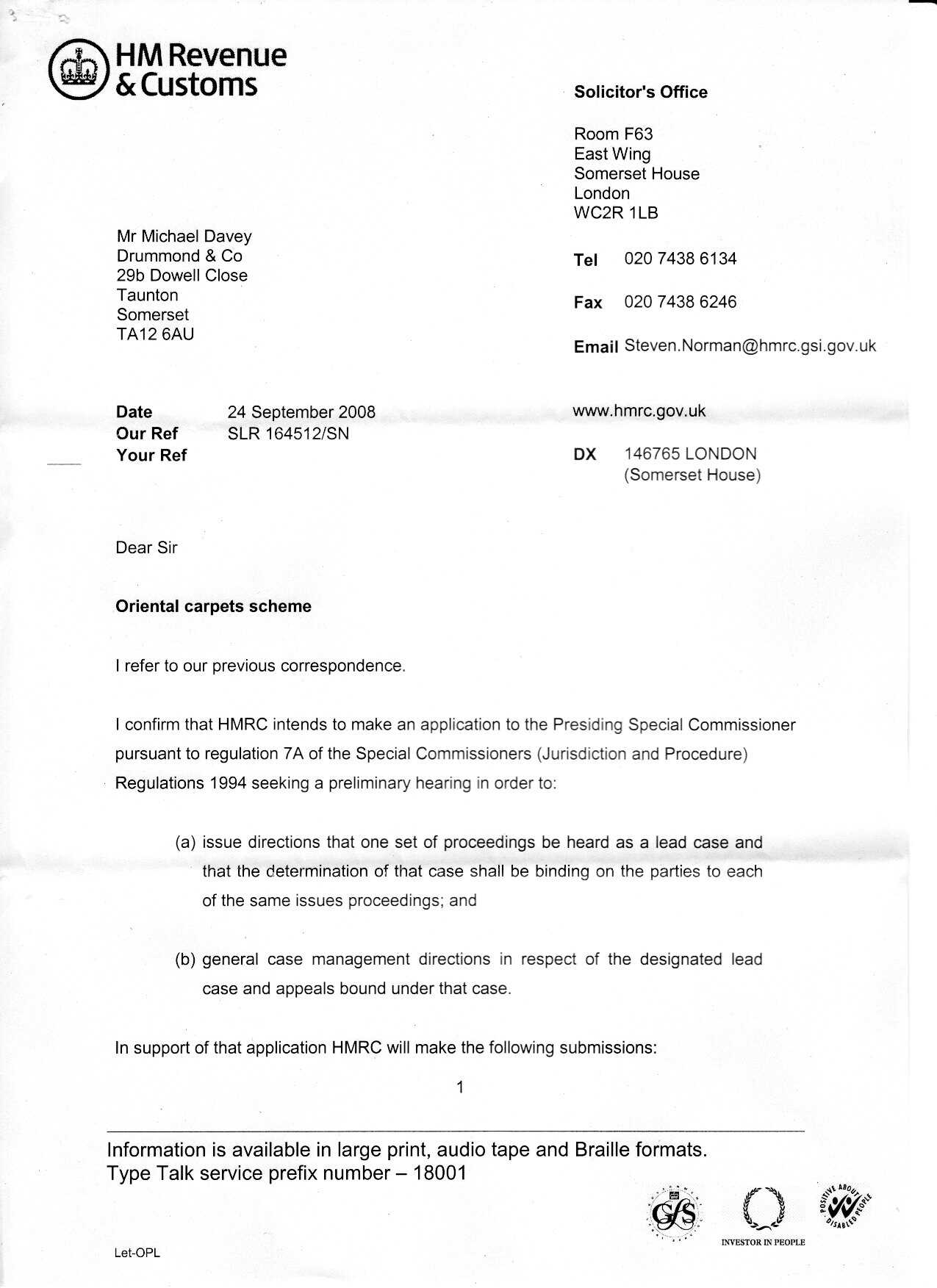

ORIENTAL CARPET AND RUG SCHEME (CROXTONS)

1. My understanding of the proposed

arrangements is as follows. An employer wishes to pay a bonus to an

employee in Oriental Carpets rather than in cash. The employer

purchases the Carpets from a dealer. The Carpets are in a bonded

warehouse. The Board of Directors of the employer company then decide

to transfer certain Carpets to certain employees by way of bonus. The

employee is informed that he will receive his bonus in Oriental Carpets

which he may have delivered, keep in bond or sell. The employer

transfers ownership in the Oriental Carpets to the employee. The

employee is then free to keep the carpets or sell them to anyone

including, of course, the dealer from whom the Carpets were originally

purchased.

2. I shall deal with the various taxes

under

individual headings.

National Insurance Contributions

3. National Insurance Contributions

("NICs")

are charged on "earnings". This is defined, for NIC purposes, as

including:

"...........any remuneration or profit

derived from an employment........."

Social Security Contributions and

Benefits Act 1992 section 3 (1).

Thus the receipt of the Carpets, being a

"profit", would be part of the employee's "earnings". However Regulation

19 (1) of the Social Security ( Contributions ) Regulations 1979

provides:

" For the purposes of earnings-related

contributions, there shall be excluded from the computation of a

person's earnings in respect of any employed earner's employment any

payment in so far as it is -..............(d) any payment in

kind......."

In my opinion, the transfer of Oriental

Carpets, under the scheme outlined in paragraph 1 above, would be a "

payment in

kind " for the purpose of this Regulation. In this regard it is very

important that:

( i ) the employee never has a choice

between the Oriental Carpets and a cash sum, otherwise there is a

danger that, on the basis ofHeaton v Bell (1969) 46 TC 211,

the employee would be treated as being paid remuneration ( rather than

a benefit in kind) equal to the cash entitlement foregone;

( ii ) the employer does not discharge any

liability of the employee, otherwise the discharge would be treated as

a payment of earnings in cash: R v DSS ex parte Overdrive Credit

Card Ltd [ 1991 ] STC 129;

( iii ) the asset is not capable of being

surrendered or exchanged for cash, as opposed to being turned into cash

by sale; and

( iv ) title to the Carpets passes from the

employer to the employee before the employee sells the Carpets for cash.

I am satisfied that none of these

difficulties would arise with the arrangements as described in

paragraph 1 of this Opinion.

4. I can, however, see two possible

difficulties with the proposed arrangements. The first is Regulation

21(2) of the Social Security ( Contributions ) Regulations 1979.

This provides:

" With a view to securing that liability

for

the payment of earnings related contributions is not avoided or reduced

by

a secondary contributor following in the payment of earnings any

practice

which is abnormal for the employment in respect of which the earnings

are

paid ( hereinafter referred to as an "abnormal pay practice " ) , the

Secretary of State may, if he thinks fit, determine any question

relating to a person's earnings -related contributions where any such

practice has been or is being followed, as if the secondary contributor

concerned had not followed any abnormal

pay practice, but had followed a practice or practices normal for the

employment

in question. "

It might be argued that, because of the

exemption given by Regulation 19 (1) , the employer is not making a

"payment of earnings" so that Regulation 21 (2) cannot apply. However ,

I find that argument unconvincing. The transfer of the Carpets is a

payment of earnings withinSSCBA 1992 section 3 ( 1 ).

Regulation 19 (1 ) simply provides that certain payments

are to be "excluded from the computation of a person's earnings in

respect

of any employed earner's employment ". It does not restrict the scope

of

the definition in section 3 ( 1 ). It is my opinion, therefore that one

cannot

safely assume that as a matter of law Regulation 21 (2 ) has no

application

to payments in kind. This, of course, leaves the question of whether

this

particular payment is an abnormal pay practice for the employment

concerned.

5. As a practical matter the Regulation 21

(2) power is not often ( if ever ) exercised by the Contributions

Agency. In particular, it has never been employed to counter any of the

schemes involving payments in kind. In recent years the approach has

been to legislate against specific forms of payment. Therefore, I would

not be concerned about a possible application of Regulation 21 ( 2 ) to

these arrangements.

6. The second possible difficulty is the

principle of statutory construction ( " the new approach " ) set out in

WT Ramsay v IRC (1982 ) 54 TC 101 and Furniss

v Dawson (1984) 55 TC 324 as explained in Craven v White

(1988) 62 TC 1. This principle could apply if the Carpets were

allotted to the employee and sold back to the supplier in a

pre-arranged series of transactions so that it was a " practical

certainty " from the start that the employee would simply receive cash

at

the end of the day. The effect of this principle applying would be that

the

NIC legislation would operate as if the employee had been paid in cash.

If

, however, the employees genuinely become owners of specific Oriental

Carpets

and are truly free to decide how they deal with these Carpets, I do not

think

that the new approach could be invoked to attack the arrangements.

Again,

in practice, the Contributions Agency have never invoked the Ramsey

principle

in relation to any arrangements involving payments in kind.

Income Tax

7. The Oriental Carpets will be an

emolument

of the employee's employment, under TA 1988 section 19,

because it is convertible into money : Tennant v Smith 3 TC 158.

therefore, although it is a benefit in kind, it is not taxed under TA

1988 section 154 because this section only applies where the benefit is

not otherwise chargeable to tax: see section 154 ( 1 ) ( b ). This does

not, of course, in any way affect the fact that the transfer of the

Oriental Carpets is a " benefit in

kind " for the purposes of the NIC legislation. Although it is an

emolument, it is important to consider whether it is subject to the

PAYE Regulations (SI 1973/334 ).

8. It is my understanding that the dealer

is

prepared to purchase the Carpets from the employee at the market price

of

those Carpets. in other words, he will pay exactly what he would pay

any

third party who was offering to sell him the same carpets. The employee

is,

of course, free to keep the Carpets or to sell them to another dealer,

or

by auction, if that would realise him a better price. There is a ready

market

in the kind of Carpets which the employee will receive. in practice,

however,

the price of Oriental Carpets is very stable and so the employee is

likely

to receive almost exactly the price which the employer originally paid

for

the Carpets.

9. The transfer of Oriental Carpets from

the

employer to the employee is clearly not a " payment " on general

principles

for the purposes of the PAYE Regulations. However the Finance

act 1994has introduced new provisions which govern the

transactions which are caught by

the PAYE Regulations. section 127 has introduced a new

section203F into TA 1988 which provides :-

" (1) where any assessable income of an

employee is provided in the form of a tradable asset, the employer

shall be treated, for the purposes of PAYE Regulations, as making a

payment of that income of

an amount equal to the amount specified in sub-section (3) below.

(2) For the purposes of sub-section (1)

above " tradable assets " means -

(a) any asset capable of being sold or

otherwise realised on a recognised investment exchange ( within the

meaning of theFinancial Services Act 1986 ) or the

London Bullion Market ;

(b) any asset capable of being sold or

otherwise realised on any market for the time being specified in PAYE

Regulations;

and

(c) any other asset for which, at the time

when the asset is provided, trading arrangements exist. "

Oriental Carpets are not covered by (a)

and,

as yet, no regulations have been issued under (b). therefore, one must

consider whether the Carpet transaction, as outlined above, falls

within (c). The term

" trading arrangements" is defined by the new TA 1988 section

203K

(2) (a): -

"(2) Trading arrangements -

(a) for an asset, are arrangements for the

purpose of enabling the person to whom the asset is provided to obtain

an amount similar

to the expense incurred in the provision of the asset."

This definition is further expanded by

section 203K (3) (b):-

"(b) an amount is similar to an expense

incurred if it is greater than, equal to or not substantially less than

that expense."

One must assume that it is very likely that

the amount which the employee will realise by selling the Carpets to

the dealer will not be substantially less than the expense incurred by

the employer in

purchasing the Carpets. The only question is whether the employee

obtains that amount by reasons of an " arrangement ".

10. This is obviously a case which is close

to the line. An argument may well be mounted by the Revenue that there

is an arrangement because the employee is pointed in the direction of

the dealer who will, in practice, always buy back the Carpets for a

predictable price. However, it seems to me that this is caused by the

nature of the market in Oriental Carpets, in particular its stability,

rather than any "arrangement". The term "arrangement" in section 6

(3) of the Restrictive Trade Practices Act 1956 was considered

by Diplock LJ. in Re British Basic Slag

Limited's Agreement [1963] 2 AER 807, where he said , at819

:-

" Cross J. said: "...... all that is

required to constitute an arrangement not enforceable in law is that

the parties

to it shall have communicated with one another in some way and that as

a

result of the communication each has intentionally aroused in the other

an

expectation that he will act in a certain way". I think that I am only

expressing

the same concept in slightly different terms if I say without

attempting

an exhaustive definition, for there are many ways in which an

arrangement

may be made, that it is sufficient to constitute an " arrangement "

between

A and B, if (i) A makes a representation as to his future conduct with

the

expectation and intention that such conduct on his part will operate as

an

inducement to B to act in a particular way; (ii) such representation is

communicated to B, who has knowledge that A so expected and intended,

and (iii) such representation of A's conduct in fulfilment of it

operates as an inducement, whether among other inducements or not, to B

to act in that particular way."

In my view Diplock LJ, is envisaging a

situation in which A's future conduct is conditioned by the informal

agreement or

understanding with B. In the present case, the dealer is not arranging

to

do anything in particular. at most the employer and (perhaps) the

employee

are informed that the employee will in practice be able to sell the

Carpets

back to the dealer because the dealer is generally in the market to buy

that

type of Carpets and further that the price is almost certain to be,

say,

£500 a piece, if the sale takes place within a week or so of the

original

purchase, due to the stability in the market for Oriental Carpets. In

my

opinion, that does not amount to an "arrangement" allowing the employee

to

obtain an amount similar to the expense incurred by the employer in

acquiring

the Carpets. it is crucial to this view that the dealer can establish

by

evidence that he actually bought similar Carpets from third parties on

the

same terms that he bought them from employees within the scheme.

11. these arrangements are certain to be

closely scrutinised and probably challenged by the Revenue. there is a

serious possibility that this challenge may succeed in the Courts.

Croxtons' advertising material ought to make it clear that, while the

NIC position is clear, the PAYE position is not nearly so certain.

Employers must take their own view, based on their own legal advice, on

how to deal with the bonus in relation to PAYE. this all, however,

summarise the effect of the PAYE provisions if the Carpet payments are

caught by the new section 203F.

12. Where the payment is caught because

there are " trading arrangements", the measure of the deemed income is

set out in section 203F (30 (b) ;-

"(3) The amount referred to is -

(b) in the case of an asset for which

trading arrangements exist at the time when the asset is provided, the

amount which is obtained under those arrangements." ( my emphasis).

It seems to follow that there is only an

amount of deemed income for PAYE purposes where cash is obtained under

the trading arrangements. Therefore, there will be no PAYE liability if

the employee holds

onto the Carpets or sells them to someone other than the dealer.

13. Where there is deemed ( or notional )

income, the employer is required to deduct income tax from actual

payments of income which he makes to that employee in accordance with PAYE

regulations: TA 1988 section 203J ( 1 ). regulation 7 ( 2 ) of the

Income Tax ( Employments ) ( Notional Payments ) Regulations 1994 (

" the 1994 Regulations " ) provides:-

" The time prescribed is any occasion on or

after the time when the notional payment is made and falling within the

same income tax period, on which the employer actually makes a payment

of, or on account of, assessable income of that employee."

An " income tax period " is normally a

period from 6th of one month to the 5th of the following month: Regulation

2 ( 1 ) of the Income Tax ( Employments ) Regulations 1993.

Where the employer is unable to deduct the full amount of the tax from

cash payments in that month, the employer is obliged to account for the

tax within 14 days at the end of the month in which the notional

payment was made: TA 1988

section 203J ( 3 ); Regulation 8 ( 2 ) of the 1994 Regulations.

In

those circumstances, the employee must reimburse the employer for the

tax

for which the employer has accounted. If the employer does not do this

within

30 days of the notional payment, the tax paid by the employer is

treated as

further income of the employee assessable under Schedule E:TA

1988 section

144 ( 1 ). There is, however no provision which makes this

deemed

further income liable to PAYE.

14. As a practical matter, if an employer

is

intending paying a bonus in Carpets, he ought to take an indemnity from

the

employee for the tax which he may have to pay. He must also take an

undertaking

from the employee that he will inform the employer if and when he sells

the

Carpets to the dealer, since that action might trigger a PAYE liability.

Corporation Tax

15. The employer will obtain a deduction for

his expenditure upon the Carpets since it will be incurred in order to

provide remuneration to the employee. This is , of course, subject to

the normal restrictions

that the remuneration must be justifiable as being wholly and

exclusively

for the purpose of the employer's trade.

Pension Contributions

16. The value of the Carpets when received by

the employee will be " relevant earnings" for pensions purposes. This

is because they are emoluments chargeable to income tax under Schedule

E ( see paragraph 7 above) : TA 1988 644 (2) (a).

Value added Tax

17 When the employer transfers the Oriental

Carpets to the employee there will be a deemed supply of goods under VATA

1983 Schedule 2 paragraph 5 ( 1 ) as the Carpets will no

longer form part of the assets of the employer's business. However,

since the goods ( the Carpets

) are subject to a " warehousing regime " and the " duty point " has

not

been reached, the supply of those goods is treated as taking place

outside

the UK: VATA 1983 section 35 ( 1 ). therefore there is

no UK

VAT charge : VATA 1983 section 2 ( 1 ). There would only

be

a VAT charge if the employee were to remove the Carpets from the bonded

warehouse.

FURTHER OPINION

DAVID EWART. Pump Court Chambers, 16 Bedford Row, London, WC1R

4EB

Ist May 1995

Re : CROXTONS ORIENTAL CARPET SCHEME

1. Regulation 3(a) of the Social

Security ( Contributions) Amendment (no4) Regulations 1995 has

added a new paragraph 9c to Schedule 1A to the Social Security

(Contributions)

Regulations 1979as follows

" 9,C Any other asset, including any

voucher, for which trading arrangements exist and any voucher capable

of being exchanged for such an asset".

Regulation 3(c) of the 1995 Regulations

also

adds a new paragraph 19 to Schedule 1A in the following terms:

" 19. For the purposes of paragraph 9c of

this Schedule " trading arrangements" has the meaning assigned to it in

203K(2)(a) of the Income and Corporation Taxes Act 1988."

2. This means assets in respect of which "

trading arrangements" exist are added to the list of assets which are

not regarded as benefits in kind for the purposes of regulation

19(1)(d) of the 1979 Regulations, and so are liable to NIC. The term "

trading arrangements" is defined by reference

to the definition for PAYE purposes in TA 1988 section 203K(2)(a). This

does

not explicitly bring in further further definitions in section 203K(3).

However,

the Agency would probably argue that subsection (3) is part of the

definition

in subsection (2)(a). It would , in my opinion, be unsafe to assume

that

sub-section (3) does not apply.

3. My opinion of 27th September 1994 must

now be applied for the purposes of NIC as well as PAYE. Paragraphs 3-6

of that opinion will only apply if "trading arrangements" do not exist.

4. In paragraph 12 of my opinion, I point

out that, for PAYE purposes, the amount of the deemed Income is the

amount obtained under the trading arrangements: see section 203F(3)(b).

Therefore, there is

only a charge where cash is actually obtained under the arrangements.

However,

regulation 2(b) of the 1995 Regulations has inserted a new paragraph

(9)

in regulation 18 of the 1979 Regulations as follows:

"(a) The amount of earnings which is

comprised in any payment by way of the conferment of a beneficial

interest in any

assets, including a voucher, falling within paragraph 9c of Schedule 1A

to

these regulations and which falls to be taken into account in the

computation

of a person's earnings shall, for the purpose of earnings-related

contributions, be calculated or estimated by reference to the amount

obtainable under the trading arrangements in question as if that amount

were obtained on the day on which the beneficial interest was conferred."

This means that if there are "trading

arrangements" in existence there will be an NIC charge on the amount

obtainable under the arrangements at the time when the carpet is

transferred to the employee. This

charge will apply whether or not the employee takes advantage of the

"arrangements"

and obtains a cash sum. As a result paragraphs 12-14 of my Opinion are

not

applicable to NIC..

FURTHER OPINION

DAVID EWART. Pump Court

Chambers, 16 Bedford Row, London, WC1R 4EB

2nd May 1995

RE: CROXTONS ORIENTAL CARPET SCHEME

1. I understand that my Further Opinion of 1st

May 1995 has caused some confusion. Apart from one point the NIC

provisions on " trading arrangements" are identical to the PAYE

provisions which I dealt with in my

opinion of 27th September 1994. Therefore, rather than repeating what I

said

in that Opinion, I simply referred to the points on PAYE which could be

applied

to NIC.

2. My opinion is, on the basis of the

evidence which I have seen and heard in Conference, that the Persian

Rug scheme does not involve "trading arrangements". My reasons are set

out in detail in paragraph 10 of my opinion of 27th September. Briefly,

this is because the dealer is prepared to buy the carpets for the open

market price which he would offer to any other seller. In my view, this

does not amount to a "trading arrangement".

|

a)

That the revenue should not pursue taxes that are NOT owed, and they

should not presume without evidence. Our story goes back many years and

to this day no court of law has found in favour of Mr Hartnett and his

underlings. However he & his underlings have not been slow in

wasting taxpayer's money chasing revenue on which legally they have no

hope in collecting.

a)

That the revenue should not pursue taxes that are NOT owed, and they

should not presume without evidence. Our story goes back many years and

to this day no court of law has found in favour of Mr Hartnett and his

underlings. However he & his underlings have not been slow in

wasting taxpayer's money chasing revenue on which legally they have no

hope in collecting.

Accountancy Age Page 2

January 20th 2005

Accountancy Age Page 2

January 20th 2005

THE DIRECTOR'S CUT

THE DIRECTOR'S CUT